On the right track

ESG IN THE MIDDLE EAST

sponsored by

The urgency of addressing climate change and the global pandemic have reinforced the importance of environmental, social and governance (ESG) practices and have bolstered investors’ interest in sustainable finance in the Middle East. In recent years, the Middle East – especially the GCC – has been a focus on increasing sustainable investing despite its substantial reliance on fossil fuels. As the region continues to transition to a greener economy, governments, investors and stakeholders in the region are increasingly ensuring sustainability efforts and ESG factors are an integral part of their strategies. However, while ESG is becoming a post-pandemic essential for investors, a recent survey by Moody’s found that the GCC asset managers are still in the early stages of integrating ESG considerations into their day-to-day operations. Only 25% of survey respondents cited ESG issues as an area of important strategic focus, while half of the CIOs considered ESG to be a moderate or low priority, albeit increasing in importance. Overall, the GCC region’s diversification away from oil and gas, and the introduction of new ESG-related disclosure requirements, are expected to raise the profile of ESG issues in the region. However, GCC asset managers’ comparatively slow adoption of an ESG-led investment approach could make it harder for them to meet evolving investor expectations.

Editor's note

Back to top

Read more

The Middle East could help shape global ESG standards and regulations

taking flight

content by: fidelity

Code red for humanity: Investors can act to prevent a global climate disaster

content by: invesco

Environmental-themed ETFs offer a world of opportunities

The EU’s new sustainable disclosure regulation is making ESG investing even more attractive

SFDR’s talents draw crowds

CONTENTS:

SUNIL KUMAR SINGH

editor, Citywire Middle East

As ESG evolves, the industry will need to catch up with granular data

the push for green data

Technology is at the forefront of China’s development strategy. In its five-year plan, the government put an extra focus on propelling the tech innovation, aiming to further build the nation into a technological powerhouse. The spotlight on Chinese tech companies creates a significant opportunity for fund managers and asset allocators, but it also raises many questions. Does the Chinese venture capital (VC) market operate in a similar manner to its Western counterparts? How do tech startups become unicorns in China? And what pitfalls should investors be aware of, both politically and economically? Our expert panel discusses how investors can tap into the Chinese tech sector, looks behind the curtains of China’s tech stars and shines a light on what’s next for the sector. While the general outlook on China appears to be positive, the delegates agree that there are obstacles to overcome. But despite conflicts rumbling beneath the surface, they are confident that the Chinese tech market will continue its upward trajectory. To make the most of it, however, investors and fund managers must properly understand the region they are investing in. In other words, a starry-eyed take on the Chinese tech opportunity won’t do the trick. You need to know what you’re doing – or find someone who does.

BACK TO TOP

A leapfrog moment for the Middle East

The Middle East’s growing role in sustainable investing may give it a competitive edge in shaping global ESG standardisation. The Middle East is heading towards a more sustainable future, and just in time. Driven by growing concerns about climate change and environmental protection, the number of investors in the region – retail or institutional, sovereign wealth funds, banks and portfolio managers – using environmental, social, and governance (ESG) factors to build their portfolios has grown substantially in recent years. Today, the ESG trend has the Middle East investment community buzzing with excitement. ESG considerations are not only being increasingly factored into investments; they have also emerged as the most common approach to sustainable investing. According to the latest findings of an annual survey by HSBC, environmental and social issues have become almost universal concerns of major issuers of capital markets securities in the Middle East, North Africa and Turkey. A whopping 97% of issuers in the region who responded to the HSBC 2021 Sustainable Finance and Investing Survey said they had increased the attention that they pay to environmental and social issues over the past year. As much as 45% of issuers said that they were already seeing the impact of climate change on their business or activities – up from just 7% a year ago. Another survey, Standard Chartered’s Sustainable Investing Review 2021, shows that there is a heightened desire to leave a positive legacy in the UAE for sustainable investing, with 74% of investors in the country saying that this is important, compared with 65% overall. The UAE is on an upward trajectory when it comes to sustainable investing but its adoption rate of 57% is slightly lower than the global average of 61%. However, given the high number expressing a desire to leave a positive legacy, the UAE could overtake other markets in terms of ESG adoption, Standard Chartered’s survey suggests.

Pushing back frontiers With ESG becoming a mainstream part of traditional investment decision-making, it’s important to see how it fits within the portfolios of investors and asset managers in the region. According to Invesco’s Global Sovereign Asset Management study, as much as 50% of sovereigns in the Middle East have increased their focus on ESG as a result of the pandemic. The study, which incorporated the views and opinions of 141 chief investment officers (CIOs), heads of asset classes and senior portfolio strategists at 82 sovereign wealth funds (SWFs) and 59 central banks across the globe, who together manage $19tn in assets, said 56% of sovereigns and 43% of central banks in the region have adopted an ESG policy. According to Moody’s 2021 survey of CIOs from eight leading fund firms in the Gulf Cooperation Council (GCC) in September, asset managers in the GCC expect a solid performance over the next 12 months. Growing demand for Islamic products and investments that take ESG considerations into account will likely support fund inflows. GCC fund firms expect to build on their strong performance in 2021, with half of CIO respondents expecting double-digit growth in net inflows, and another 33% foreseeing a high single-digit increase, the ratings agency said in the survey. Respondents are bullish regarding ESG-compliant investment products, with 38% expecting a significant increase in demand for such assets. However, the survey indicates that GCC asset managers are still in the early stages of integrating ESG considerations into their operations, lagging behind foreign players. This could make it harder for GCC asset managers to meet investor expectations of ESG issues, putting them at a competitive disadvantage as foreign firms expand their presence in the region, Moody’s noted.

words by Sunil Kumar Singh

Taking flight

chapter one

Interest for sustainable investments in the UAE, and across international markets, is at an all-time high, signalling a valuable opportunity to address global climate change and environmental concerns through financial means

Challenges ahead Notwithstanding the robust investor demand, ESG investing remains a nascent asset class in the GCC region. ‘While economic development in a sustainable way is the raison d’etre for GCC asset classes, the GCC is challenged by ESG mandates as commodities remain a linchpin of many markets, social inequities remain pervasive and governance standards have been worse off,’ MUFG bank said in its report, ‘GCC region: Path towards a new economic model’. Dedicated public ESG-compliant assets in GCC fixed income remains small at around $12bn, MUFG said. However, it added that total GCC ESG issuance stands at $42bn, so demand for ESG assets goes beyond these dedicated mandates into broader investment policy decisions. ‘Whilst in infancy, GCC corporates are working with sovereigns in devising ESG strategies, investor demand has been strong and the market is willing to own them through the nominal yield curve of the issuer,’ the bank said. According to Moody’s 2021 survey, in the GCC region, ESG investing is rapidly gaining traction among investors, in line with increased awareness of ESG issues globally as a result of the pandemic. In an effort to attract ESG investment, GCC countries are taking steps to tighten sustainability reporting requirements for companies. GCC stock market operators have also put in place measures to meet the demand for ESG products. Examples include the introduction of ESG reporting requirements for listed companies by the Abu Dhabi Securities Exchange (ADX), and the Dubai Financial Market (DFM). In April 2020, the DFM launched its first ESG index, and Saudi Arabia’s Tadawul Stock Exchange said in August 2020 that it would follow suit in early 2021, although it has not done so yet.

Owen Young

Standard Chartered Bank

How can investors tap into China’s tech story?

next

previous

It’s no secret that many countries in the GCC have relied on fossil fuels for a long time to bolster their economies but it is also clear that there is a huge sea change in the offing

Gemma Woodward

Quilter Cheviot

However, the survey reveals that GCC asset managers are still in the early stages of integrating ESG considerations into their day-to-day operations. Only 25% of survey respondents cited ESG issues as an area of important strategic focus, while half of the CIOs considered ESG to be of moderate or low, albeit increasing, importance. As Owen Young, managing director and regional head of wealth management for Africa, the Middle East and Europe at Standard Chartered Bank, said: ‘Interest for sustainable investments in the UAE, and across international markets, is at an all-time high, signalling a valuable opportunity to address global climate change and environmental concerns through financial means. ‘Although investor interest in these investments has been confirmed, it is the responsibility of corporates to provide a compelling sustainability narrative that truly emphasises the positive impact of their operations on global environmental, social, and governance objectives,’ he said. At a time when economies in the GCC are seeking to diversify away from hydrocarbons, the region has an opportunity to promote its ESG values. Gemma Woodward, director of responsible investment at Quilter Cheviot, said: ‘It’s no secret that many countries in the GCC have relied on fossil fuels for a long time to bolster their economies but it is also clear that there is a huge sea change in the offing. Governments in the GCC have expediated investments in renewables, including solar and waste. This is well-illustrated by the agenda at the upcoming Dubai Expo where many of the topics that are to be explored centre around sustainability and the race to zero-carbon emissions.’ The GCC’s reliance on fossil fuels is not going to evaporate overnight but there is a clear understanding that things need to change, Woodward added.

welcome

chapter two

chapter three

Content from: invesco

Content from: fidelity

Advertisement feature

CONTENT BY

“ESG investing is often perceived as a European and US phenomenon,” explains Alessio Cirillo, Director, Invesco Middle East. “However, the pandemic and global warming have accelerated the adoption of ESG objectives amongst Middle Eastern clients who understand that incorporating ESG within their portfolios does not have to come at the expense of returns. “In many cases, clients in the Middle East are adopting these principles through the use of an ETF structure. An ETF is an efficient and low-cost investment vehicle that allows investors to gain exposure not only to broad indices but also more precise environmentally and socially responsible themes they feel strongly about, and at the same time correlates to their desired investment outcomes. Themes such as Water Resources, Clean Energy, or a more focused approach on Solar Energy are being accessed by Middle East investors who are increasingly choosing ETFs as the preferred investment vehicle for their portfolios.” Thematic ETFs enable investors to express a view more precisely than they could with a standard sector ETF. By looking beyond conventional industry classifications, or ignoring them altogether, these strategies have evolved to capture a specific set of opportunities tied closely to a given theme, such as companies involved in certain disruptive technologies or transformational developments. Anyone seeking an investment case underpinned by long-term supply and demand trends only needs to look at the world around them. Literally. The need to combat rising global temperatures and the depletion of natural resources seems destined to remain on top of political agendas and in the public eye for decades to come. Of course, this wouldn’t be the first time that a government has tried to support demand for clean energy adoption. We’ve seen subsidies offered and similarly funded initiatives trialled before, including in Europe, but they’ve always petered out. The most recent example was in the global financial crisis when governments were forced to cut spending. A lot has changed in a short space of time What’s different now? First of all, we are seeing for the first time in history the largest economies – and coincidentally the largest polluters – united in their commitment to reach carbon neutrality by 2050, or 2060 in the case of China. While each country that has signed the Paris Agreement will formalise its own plans and policies for achieving this ambitious “Net Zero” goal, they will almost certainly require a transformation of entire industries towards the use of cleaner and more sustainable energy sources, such as solar, wind, hydro and geothermal. Until recently, however, these clean energy technologies needed subsidising to be economically viable. That’s where the second, and arguably most significant, change has occurred. According to the International Agency for Renewable Energies (IRENA), 62% of the renewable power that came on-stream in 2020 achieved a lower electricity cost than new plants using the cheapest fossil fuel available. The cost of generating electricity from solar power has fallen 85% over the past 10 years. Solar is now the cheapest energy in many countries, and costs are also coming down in wind and other renewables [1]. In other words, they don’t need government funding. The costs are being driven lower by advancements in technology and economies of scale, both of which are expected to continue as capacity is ramped up across the globe. Battery and hydrogen fuel cell technologies could be higher growth areas in coming years. The former is increasingly vital for enabling the electricity to be used 24/7, overcoming intermittency issues due to lack of wind or sunlight. Complete “solar plus storage” solutions are now becoming more commonplace. Hydrogen fuel cells are in an even earlier stage of development and will be integral in decarbonising energy-intensive industries, such as shipping. It’s not all about solar panels and wind turbines Clean energy as a theme can be wider and more diversified than many people expect, whether you think about all the different types of clean energy or even if you focus on just one. For example, the solar supply chain is more than just solar panel manufacturers. It can include firms that specialise in financing huge projects and those constructing and maintaining installations, in addition to a host of companies that develop and manufacture the many different components. Solar tracking systems, for instance, have been around for a long time but are only now becoming cost-effective for certain large-scale applications. Trackers are designed to move the solar panels automatically throughout the day, so they are able to capture sunlight most effectively from dawn to dusk. Energy efficiency is an important and often overlooked area for any clean energy theme. How to gain exposure ETF investors who want exposure to clean energy can choose from strategies aiming to capture companies involved in one specific segment such as solar and others offering broader exposure. The investment universe for even the narrowest focus may still provide plenty of opportunities especially if the ETF is invested globally and across market-caps. Too much in large caps could result in being overweight overpriced stocks, so diversification can be a benefit. With most ETFs being passive vehicles, investors should be able to clearly understand the index methodology. Investors may want to ask how the underlying index defines the investment universe, as well as how stocks are selected and weighted. One methodology could be to select constituents and apply weightings based the proportion of revenues a company earns from clean energy, assigning more weight to “pure play” companies. And will the index be able to identify and capture new developments as and when they become cost-effective enough to be profitable? Clean energy is rapidly evolving, and Investors can find a world of opportunities in environmentally themed ETFs. Investment risks Investment strategies involve numerous risks. Investors should note that the price of your investment may go down as well as up. As a result, you may not get back the amount of capital you invest.

Robin Parbrook Co-Head of Asian Equity Alternative Investments

See all articles

Read more: are China's economic prospects shifting?

[1] Data from IRENA, June 2021 Important information Published by Invesco Asset Management Limited, Perpetual Park, Perpetual Park Drive, Henley-on-Thames, Oxfordshire, RG9 1HH, United Kingdom. Invesco Asset Management Limited, PO Box 506599, DIFC Precinct Building No 4, Level 3, Office 305, Dubai, United Arab Emirates. Regulated by the Dubai Financial Services Authority.

advertisement feature

As ESG evolves in the Middle East, investment strategists are faced with the paucity of granular ESG data and standardised reporting metrics. Over the past few years, ESG investments have gained greater importance among investors, policymakers, and other key stakeholders, and they are now increasingly considered a must-have within investment portfolios. In the Middle East, portfolio managers and investors are increasingly incorporating ESG considerations into their investment approaches. However, the biggest challenges for asset managers, CIOs and investment strategists are to define exactly what ‘green’ investments are and how to integrate ESG data, which is not easily available, into their portfolio analysis. This was one of the key discussion points of the virtual roundtable discussion organised recently by Citywire Middle East. One of the key issues during the discussion was how investment strategists and portfolio managers can better integrate ESG data into their portfolios. The roundtable was hosted by a panel of distinguished speakers, which included Chafic Jabbour, senior executive officer and head of MENA at Candriam; Chris Langner, director and acting head of investment strategy at First Abu Dhabi Bank; Maurice Gravier, CIO of wealth management at Emirates NBD; and Kishore Muktinutalapati, equity strategist at Abu Dhabi Commercial Bank. The discussion went beyond the buzz of ESG investing and explored its various nuances, ramifications and challenges, especially in the context of the Middle East region, where there has been significant traction around sustainability and ESG investing over the past few years.

Due diligence For one, the panellists agreed there is no one best way to integrate ESG and that there is a lack of standardisation and consistency in ESG terminology. As a result, in the absence of common standards and regulations, it becomes difficult to compare and aggregate the performance of a fund or a portfolio. Another related concern the panellists raised during the discussion dealt with the lesser availability of publicly available or granular ESG data. Given these challenges, how can the industry truly measure and compare funds based on ESG criteria and how are investment managers dealing with the scarcity of ESG data? ‘That’s a debate that goes way beyond the Middle East. There is a variety of not only metrics for ESG but also the understanding of what is green,’ Chris Langner, director and acting head of investment strategy at First Abu Dhabi Bank, said during the roundtable. ‘It's easier to say what is good governance and there is a very good standard about that. Good social [critiera] is probably a little bit more up in the air as well. But the “E” part, which we have woken up more intensely to recently, is the hardest one to pin down and say, “well, this is really green”. ‘So what is ESG? Well, you have to select the companies that have it in their DNA, that are big enough to invest in it, that believe in it, that are taking it forward, and that are looking intergenerationally,’ he said. Likewise, Maurice Gravier, CIO of wealth management at Emirates NBD, said: ‘If you do wealth management in a transgenerational way, naturally, you take into account the various financial risks, whether you have the ESG data or not. So, let’s go above ESG data when you don’t have it.’ Gravier said that there are two things that make an investment sustainable. The first is that it has to be a good investment. ‘We first look at the business and the business attributes themselves,’ he said. According to Kishore Muktinutalapati, equity strategist at Abu Dhabi Commercial Bank, the best strategy for fund selectors is to avoid greenwashing. However, he said a bigger hurdle is a lack of consensus on benchmarks. ‘The bigger issue is considering benchmarks. What would you consider [to be] benchmarks and peer groups in your industry? That is a big debatable question,’ he said, adding that fund selectors need to be aware of these issues and then develop an internal framework in which they can look at the products.

The push for green data

The development of the ESG ecosystem is already underway, with participation coming from governments, corporates and investors themselves, which is unstoppable

Evolving ecosystem So, isn’t it high time regulators, investors and other stakeholders in the Middle East came together to draft the region’s own set of ESG standardisation? ‘The development of the [ESG] ecosystem is already underway, with participation coming from governments, corporates and investors themselves, which is unstoppable. Hopefully, things will be in place relatively soon,’ said Muktinutalapati. Gravier said that the UAE has been at the forefront of everything related to ESG, sustainability, energy transition, and gender parity. ‘I trust innovation and sustainable capitalism to bring solutions to everything. We are very lucky to live in the UAE where we see these dynamics everywhere,’ he added. Chafic Jabbour, senior executive officer and head of MENA at Candriam, said: ‘While greenwashing is all over the place, when you look at the company’s track record, engagement and commitment, this is where you come to know who is actively engaged in ESG. ‘And this is what SFDR regulations are supposed to put forward to differentiate between asset managers that just feed information in general and those [that] are totally committed to ESG.’ Overall, the speakers agreed that ESG is more than a feel-good factor, and from a nice-to-have investment, ESG has become a must-have for a significant number of investors. The formalisation of ESG has had a long-lasting impact on how sustainability factors are incorporated into investment decisions. As the green push continues across the region, the next challenge will be how to maintain standardisation. This will need to be a combined effort from financial market regulators, investors, and other industry stakeholders.

Kishore Muktinutalapati

Abu Dhabi Commercial Bank

A matter of style

‘I trust innovation and sustainable capitalism to bring solutions to everything. We are very lucky to live in the UAE where we see these dynamics everywhere

Maurice Gravier

Emirates NBD

Code Red for Humanity: Investors Can Act to Prevent A Global Climate Disaster

[1] Source: MaxPlanck Research ‘Hot Air in the Orient’ www.mpg.de/10856695/W004_Environment_climate_062-069.pdf [2] Source: Goldman Sachs, 13 October 2020 Disclaimer This information must not be reproduced or circulated without prior permission. Fidelity International refers to the group of companies which form the global investment management organisation that provides information on products and services in designated jurisdictions outside of North America. This communication is not directed at, and must not be acted upon by persons inside the United States and is otherwise only directed at persons residing in jurisdictions where the relevant funds are authorised for distribution or where no such authorisation is required. It is your responsibility to ensure that any service, security, investment, fund or product outlined is available in your jurisdiction before any approach is made to Fidelity International. Unless otherwise stated all products and services are provided by Fidelity International, and all views expressed are those of Fidelity International. Fidelity, Fidelity International, the Fidelity International logo and the F symbol are registered trademarks of FIL Limited. The DIFC branch of FIL Distributors International Limited, is regulated by the DFSA for the provision of Arranging Deals in Investments only. The branch is established pursuant to the DIFC Companies Law, with registration number CL2923, as a branch of FIL Distributors International Limited, registered in Bermuda. FIL Distributors International Limited is licensed to conduct investment business by the Bermuda Monetary Authority. All communications and services are directed at Professional Clients only, persons other than Professional Clients, such as Retail Clients, are NOT the intended recipients of our communications or services. Investments should be made on the basis of the current prospectus and KIID (key investor information document), which are available along with the current annual and semi-annual reports free of charge from our distributors. This document makes reference to a Fund which is not subject to any form of regulation or approval by the Dubai Financial Services Authority (“DFSA”). The DFSA has no responsibility for reviewing or verifying any documents in connection with this Fund. Accordingly, the DFSA has not approved this document nor taken any steps to verify the information set out in therein, and has no responsibility for it. The Units may be illiquid and/or subject to restrictions on their resale. Prospective purchasers should conduct their own due diligence on the Units. If you do not understand the contents of this document you should consult an authorised financial adviser.

Velislava Dimitrova Portfolio Manager, Fidelity International

Visit gsam.com

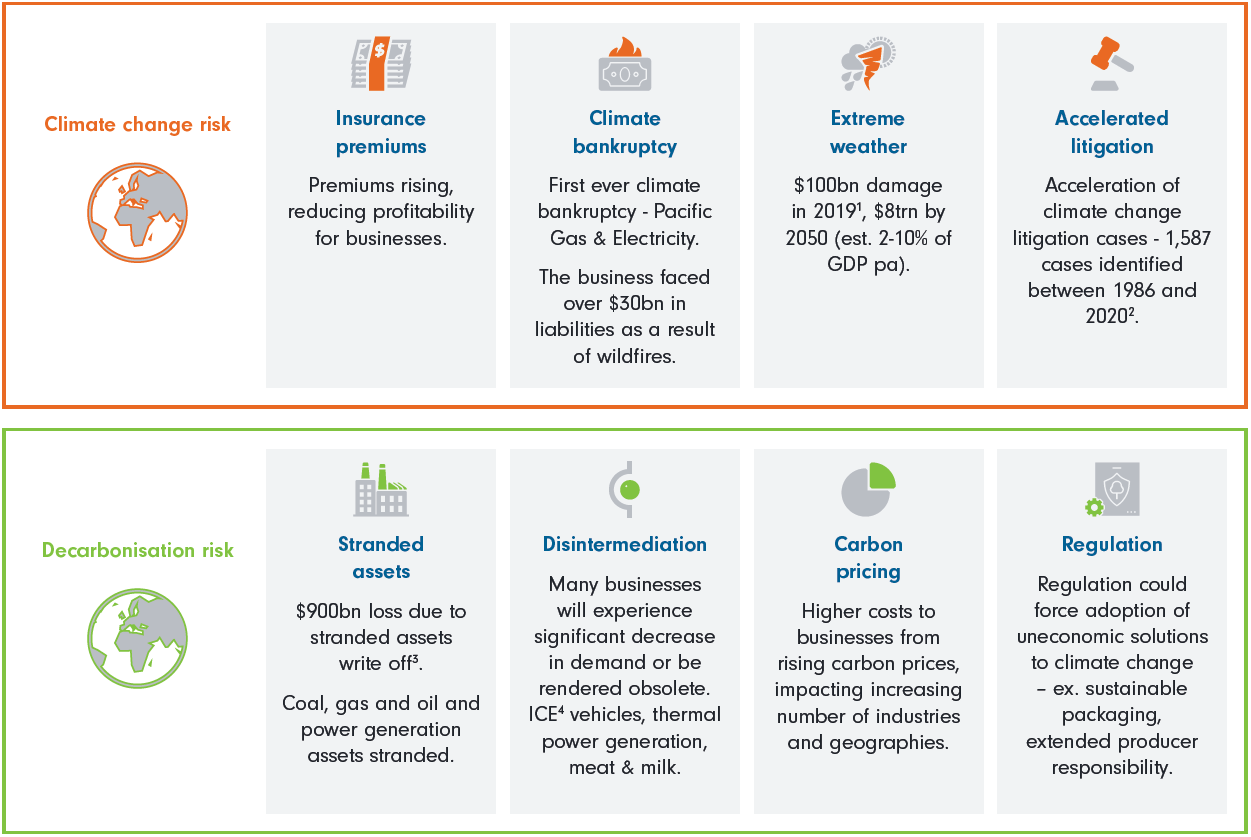

Governments, corporations and society as a whole widely acknowledge that climate change is one of the greatest challenges facing the global economy and our way of living. In order to prevent disastrous socioeconomic consequences, the Paris Agreement recommends limiting global warming to 1.5°C above pre-industrial levels. To achieve this, global emissions must fall by 50% by 2030 and 100% by 2050. In the Middle East, it is predicted that by 2050, temperatures will be 4% higher [1]. By the end of the century, there will be 200 days of extreme heat every year, making some cities in the region uninhabitable. Emissions have never fallen outside of recessions and the scale of reduction necessitates a radical transformation of the global economy. This will not come without a price; to fully decarbonise the global economy by 2050 will require an investment of around 7x US GDP ($144 trillion) into decarbonisation solutions [2]. With less than 30 years to achieve global decarbonisation, investors need to play a vital role in accelerating the adoption of decarbonisation solutions. Solutions that can enable global decarbonisation of more than 80% already exist today, but they need to be adopted more widely. This can be achieved through the financing of decarbonisation solutions, which will help achieve scale, reduce technological costs, and lower the cost of capital for new technologies. Active decarbonisation – not carbon avoidance – The solution Carbon avoidance is not the answer, and neither is mild carbon reduction. Investing in low-emissions sectors such as financials and consumer, or companies that are reducing their carbon footprint only provides a modest contribution to cutting emissions. To drive decarbonisation, investors must support and accelerate the adoption of solutions that provide step-change reductions in society’s emissions. It is companies investing in low carbon technologies that will provide the solutions to decarbonise all aspects of our lives. Climate solutions can protect against financial impact While the transition to a low carbon society will span decades, it may leave some business models obsolete and impact multiple industries. Investing in climate solutions could therefore offer protection from both climate change risk and decarbonisation risk associated with global warming. Climate change and decarbonisation risks

Source: Fidelity International, 31 May 2021 [1] Guardian 2020, Fidelity analysis 2021 / [2] Setzer and Rebecca Byrns, 2020 / [3] Financial Times, 2020 / [4] ICE stands for Internal Combustion Engine.

Looking at the bigger, greener picture To combat climate change, we have identified several investable decarbonisation themes, which include the replacement of internal combustion engines with electric vehicles, the shift from fossil fuels towards renewable power generation, the circular economy (recycling), shifting consumer patterns, and improvements to create more environmentally efficient infrastructure. As this is a nascent and fast-evolving area, the investment universe continuously expands as new technologies become investable. If each of the major decarbonisation technologies were already fully adopted globally, CO equivalent emissions would be 80% lower. This is far from the case now, which means that the transition to a low carbon world will be a multi-decade megatrend that is in its early stages. This being said, the adoption of decarbonisation technologies is accelerating, led by government subsidies, regulation, changing consumer attitudes and investor appetite. Through the help of governmental subsidies, many of these technologies, such as renewables, have already reached economic viability, which will enable wide scale adaptation and present an attractive market for investors due to strong end market demand. However, other decarbonisation solutions, such as green hydrogen and electric vehicles, still require significant investment to become economic and reach wide scale adoption. Investors therefore have a significant role to play, to deploy capital towards decarbonisation solutions and facilitate economies of scale and subsequent wide scale adoption. To create long-term impact, investors must look at companies investing in and facilitating low-carbon technologies, including those within the higher carbon intensive sectors (such as industrials, energy and utilities) where there is the greatest scope for large-scale improvements. Furthermore, investors have a responsibility to engage and encourage adoption of carbon reduction strategies and climate-related governance structures. Tackling one of the biggest challenges facing the global economy in the next thirty years may also prove to be one of the most rewarding investment opportunities over this time. Taking Action For investors looking to take concrete steps to help avert a climate disaster and at the same time find potentially profitable opportunities in a multi-decade investment trend, Fidelity has the Sustainable Family of Funds to meet their needs. In particular, the Fidelity Funds (FF) - Sustainable Climate Solutions strategy addresses the climate crisis head-on in seeking solutions to combat climate change. Unlike other funds in the climate arena that seek to benefit from climate change or merely avoid carbon intensive sectors, what sets the FF - Sustainable Climate Solutions Fund apart is its focus on solutions that actively help to decarbonise society. It provides a mechanism to support adoption of existing and emerging solutions that can help to reduce carbon emissions, while seeking to capture the structural growth opportunities that decarbonisation will provide. The benefits of such an approach is that it allows for diversified exposure across a range of technologies, sectors and business models and reduces single-technology risk which is inherent in focused solutions such as clean energy or electric vehicle funds. The FF - Sustainable Climate Solutions Fund offers a broad investment opportunity set in transportation (electric vehicles, fuel cell vehicles, ride pooling), power (renewables, green hydrogen), industry (agricultural efficiency, cloud/5G infrastructure, carbon capture and storage), buildings efficiency and consumer (recycling, alternative meat/milk, remove work/healthcare). At Fidelity, ESG analysis is integrated into our rigorous fundamental stock selection process. We actively engage with companies on a wide range of issues, including their impact on the environment, to foster positive change and enhance long-term value for investors. As stewards of investors’ capital and a provider of sustainable investment, we hold ourselves accountable for our impact on society and the environment. Fidelity has this year brought forward by 10 years our commitment to reduce our own carbon emissions to net zero by 2030. We are facing a climate crisis that demands immediate, collective action. As Anne Richards, our Chief Executive Officer, puts it: “Tackling climate change quickly is hard, but if we work together, we can make a difference.” To find out more about Fidelity’s Sustainable Family of Funds, click here.

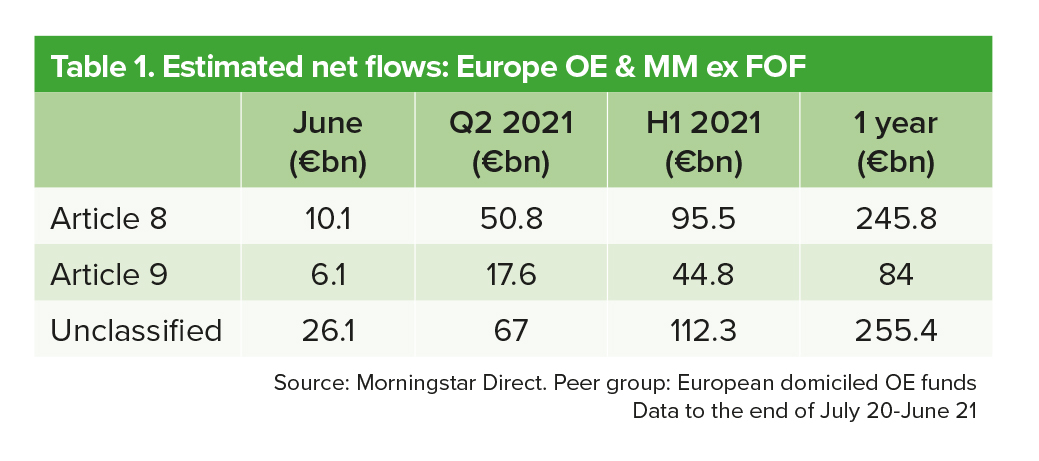

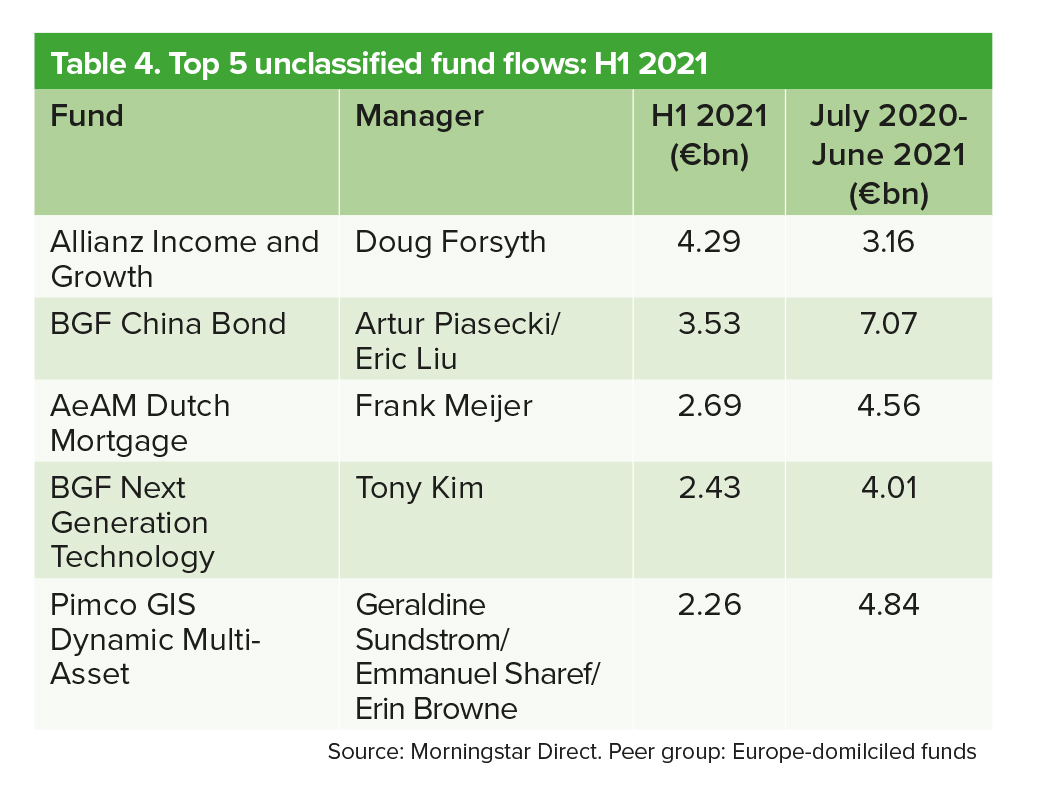

2

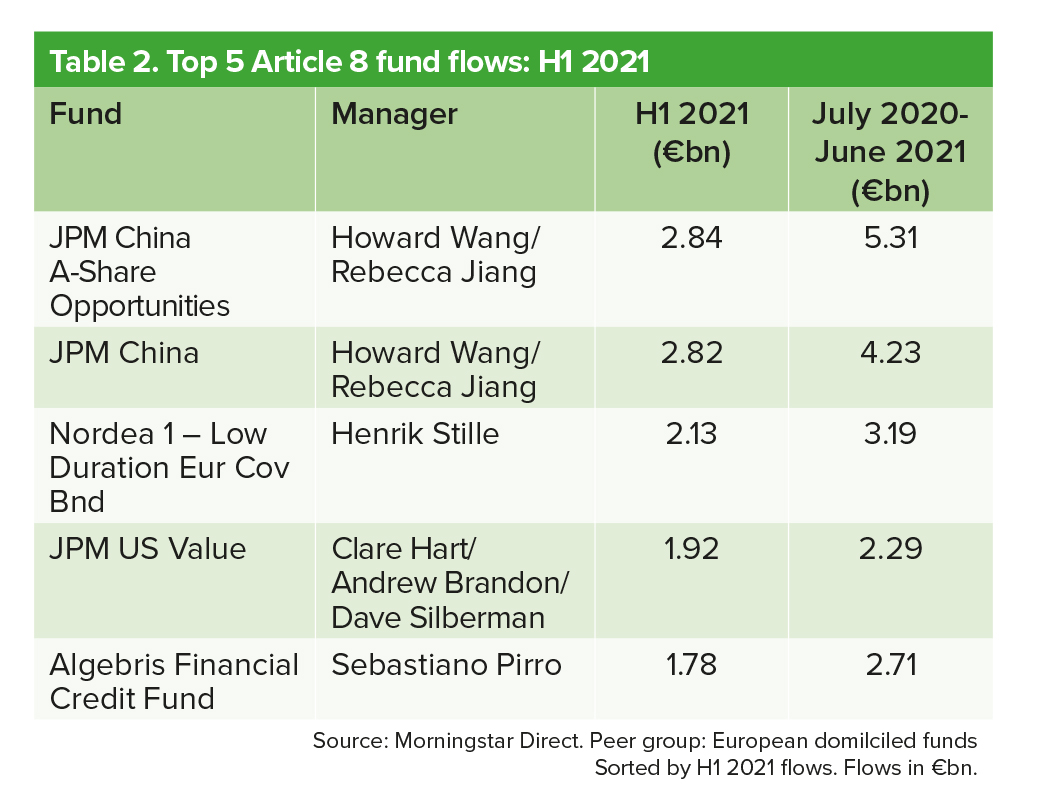

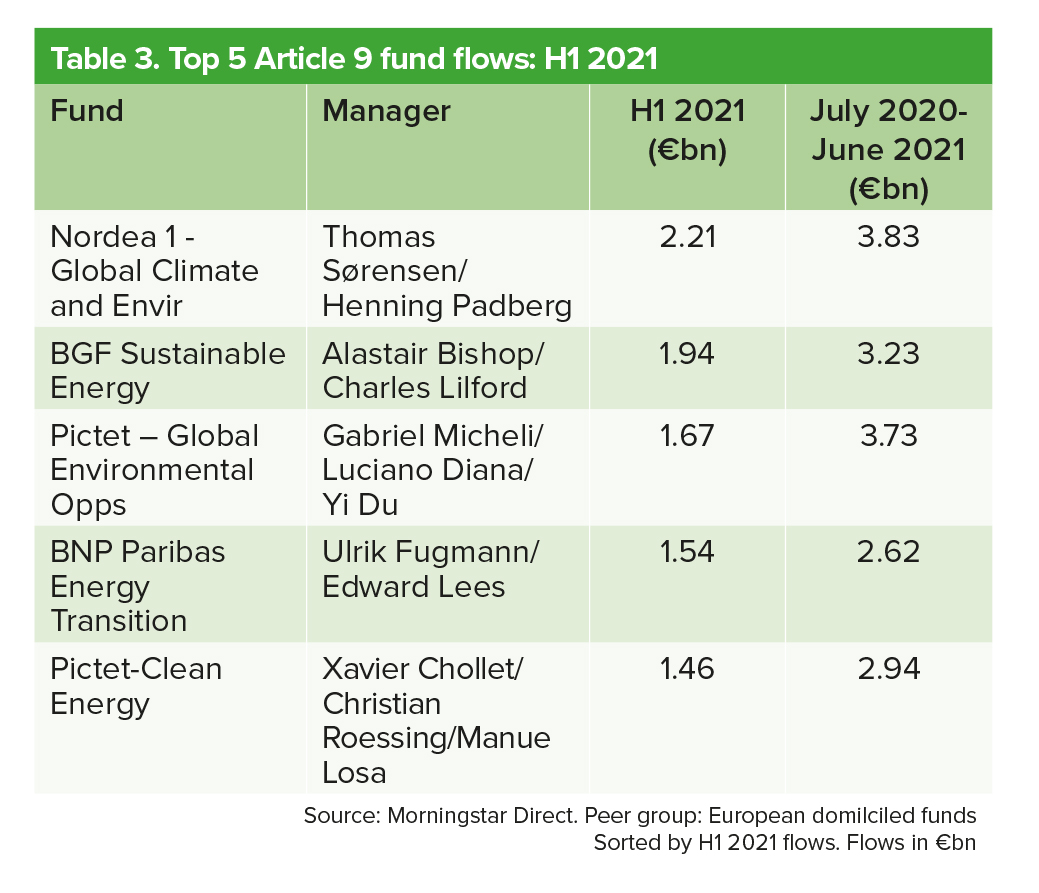

The EU’s new sustainable disclosure regulation is making ESG investing even more attractive to investors, who now have the information they need to make choices in line with their sustainability goals. To eliminate greenwashing and increase transparency, firms must now adhere to the EU Sustainable Finance Disclosure Regulation (SFDR) and make certain declarations and disclosures about the impact their funds and other financial products have on the environment. It is hoped the SFDR will drive investment decisions towards greener industries, businesses and projects. The SFDR classifies funds in three categories, as laid out in Articles 6, 8 and 9. Article 6 denotes funds that do not have a specific ESG objective and do not integrate any kind of sustainability into the investment process. They can include stocks that are excluded from ESG funds, such as tobacco and coal producers, and should be clearly labelled as non-sustainable. Article 8 covers ‘light green’ funds, which promote environmental and social characteristics but do not have them as the main objective. The categorisation applies ‘where a financial product promotes, among other characteristics, environmental or social characteristics, or a combination of those characteristics, provided that the companies in which the investments are made follow good governance practices’. Article 9 covers funds that have sustainable goals as their objective. These ‘dark green’ funds may invest in companies where the goal is to reduce carbon emissions. In these instances, the fund manager may be required to track an EU climate transition benchmark. Additionally, these funds must ‘do no significant harm’ and align to at least one of the criteria outlined in the Taxonomy Regulation. The SFDR was introduced on 10 March 2021, and there has since been a much-needed ironing out of the technical details. A further 13 regulatory technical standards, referred to as SFDR Level 2, were to be introduced on 1 July. However, their introduction will now take effect from 1 January 2022, meaning fund managers have an additional six months to implement the standards. Here, using Morningstar data, we look at the flows and performance of funds that have been classified into Articles 8 and 9 and compare them to funds that have not yet been classified. Flows At the end of June, there were 4,064 Article 8 funds, 514 Article 9 funds and 14,616 not-stated funds (funds that are unclassified). The amount of money going into Article 8 funds is staggering. The 4,064 funds have taken in €245.8bn over the year to the end of June, while the 14,616 unclassified funds have taken in €255.4bn. The rush to invest in ESG-related funds accelerated during the pandemic, with most of the money going into strategies within the ecology and renewable energy sectors. Article 9 funds saw a surge in flows into individual strategies, including the Nordea Global Climate and Environment fund, which took in €2.21bn in the first half of this year, and the Pictet Global Environmental Opportunities fund, which took in about €3.73bn over the year to the end of June. What may come as a surprise is the presence of Chinese equities among some Article 8 funds. China has a poor track record in ESG measures, particularly when it comes to state-owned companies, including substandard treatment of workers, second-rate health and safety conditions, and myriad human rights violations. The Chinese equities in Article 8 funds will have addressed these social issues. JPM Asset Management fund managers Howard Wang and Rebecca Jiang, both of whom are Citywire AAA-rated, have been top flow takers over the past year. Their JPM China A-Share Opportunities and JPM China funds have accumulated combined net inflows of €9.54bn over the past year.

words by Dr Nisha Long

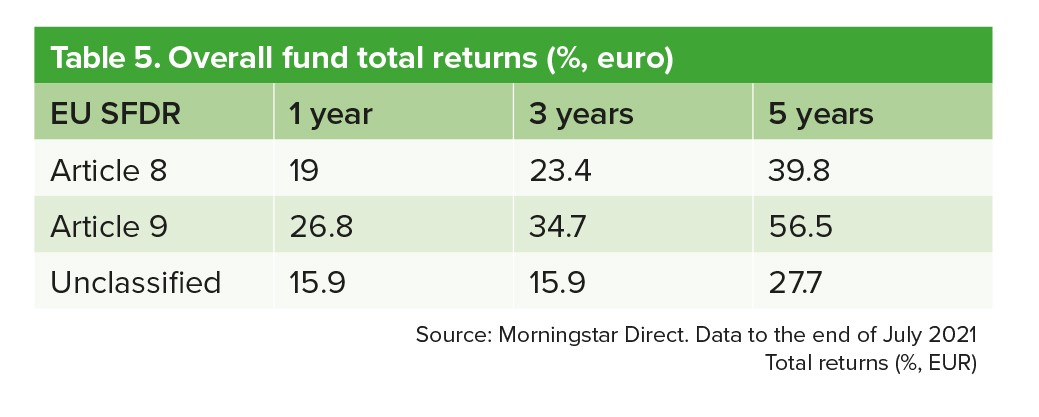

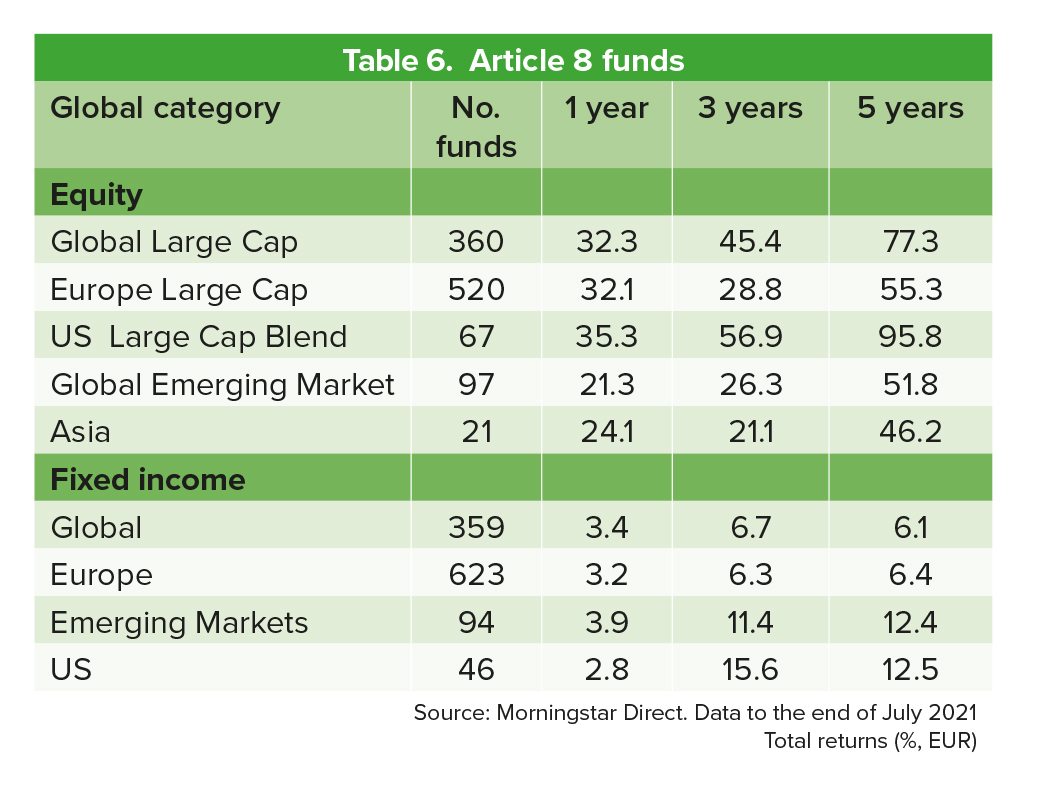

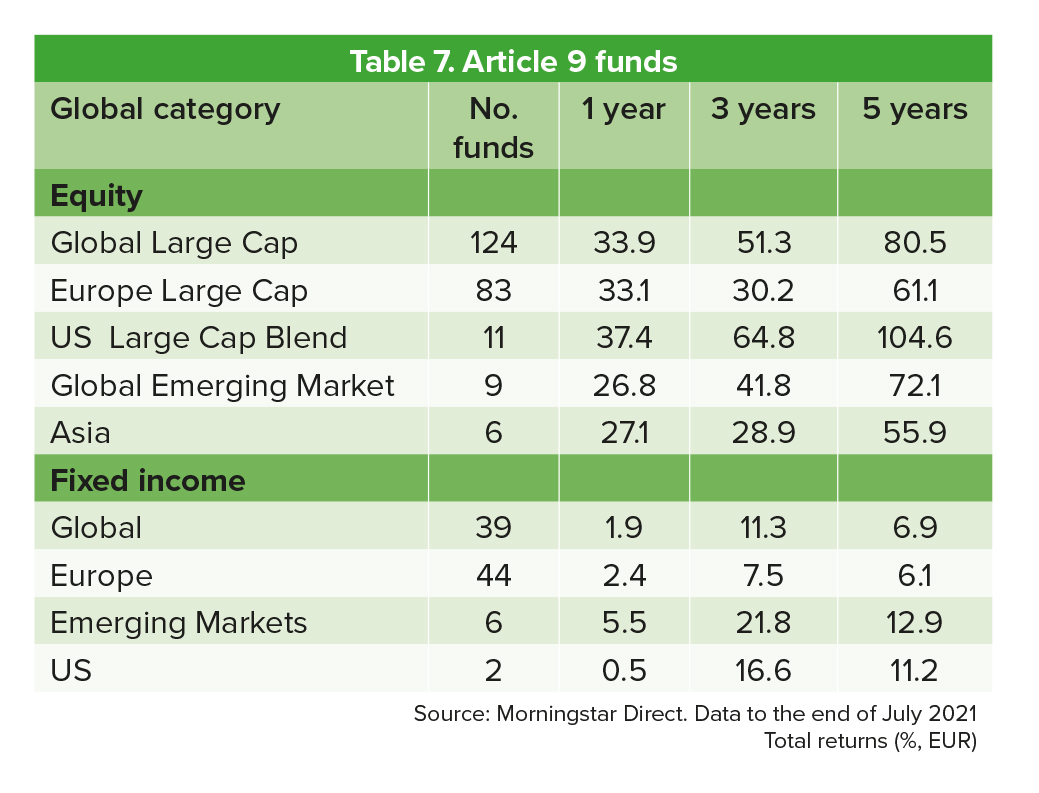

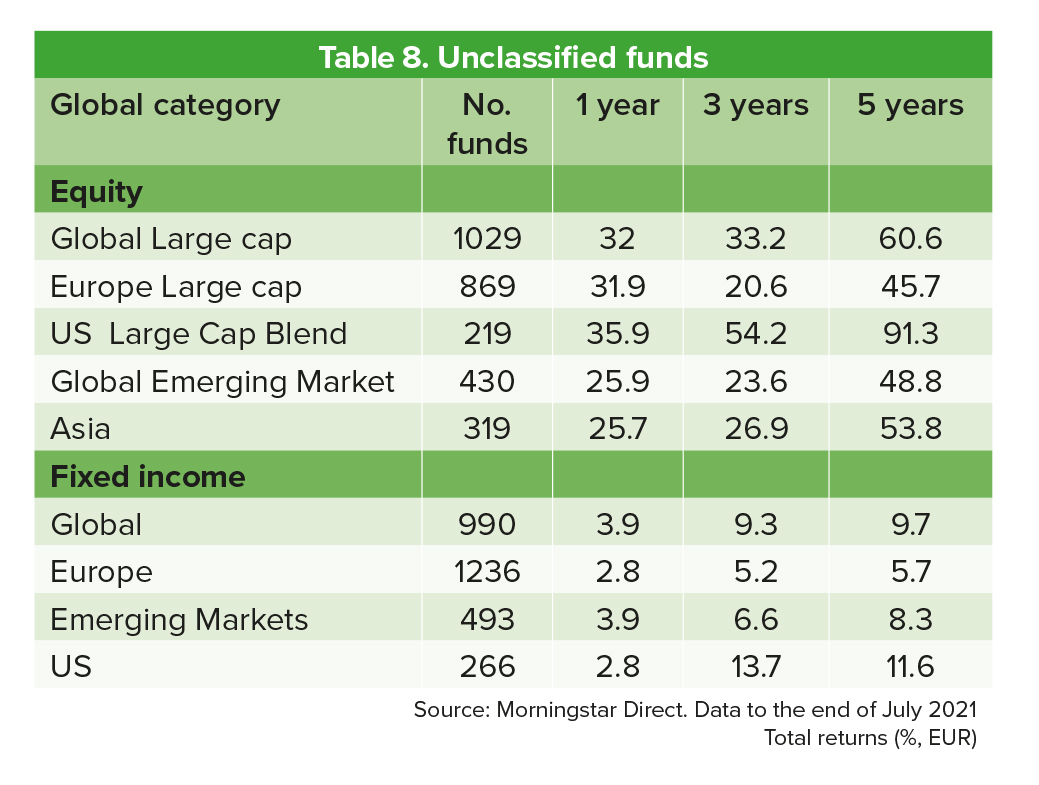

Performance In 2020, by comparing funds labelled ESG and non-ESG in the same fund group, I showed that ESG funds were able to outperform non-ESG funds during the pandemic. There is a notion that investors sacrifice returns by investing in ESG-labelled strategies. However, the data presented in tables 5 to 8 show otherwise. Comparing equity and fixed income categories, the overarching finding is that Article 9 funds deliver higher returns in comparison to Article 8 funds and unclassified funds. It is a myth that returns are sacrificed by choosing ESG funds. Equities In the global large-cap equities category, which includes value, growth and blend strategies, Article 9 funds returned, on average, 80.5% over the past five years. In contrast, Article 8 funds returned 77.3% and unclassified funds returned 60.6%. The gap is wider for global emerging markets, where Article 9 funds returned 72.1% on average compared to an average of 51.8% for Article 8 funds and 48.8% for unclassified funds. This trend is also seen in the other categories of equities. Fixed income Findings are dispersed for fixed income strategies over the past five years. This is not surprising as the reporting of ESG-related disclosures for fixed income strategies lags those of equities. The main lag comes from government bonds. Having said that, Article 9 fixed income funds have outperformed Article 8 and unclassified funds over the past three years quite handsomely. In emerging markets, in particular, having strong ESG requirements gives better outcomes. Emerging markets are known for focusing less on ‘S’ and ‘G’ issues. Historically, it has been found that governance can be poorer in emerging world companies. However, investors are taking a stand and investing in companies where controversies are rare. Reputational damage can affect the bottom line for a company detrimentally, with investors losing faith and customers going elsewhere. Looking carefully into ESG factors bears fruit in emerging markets.

The best-performing Article 8 and 9 funds invest in the environmental side of ESG, with ecology and renewable energy funds at the top. The best-performing Article 8 fund over the past three years to the end of June is the green benefit Global Impact fund, which returned 231.4% in euro terms. Its name suggests it is an Article 9 fund. However, it is classed as an Article 8 fund with some ESG considerations. The best-performing Article 9 fund over the same period is the LSF - Active Solar fund, which returned 229.7%. The fund invests in solar energy and has benefited from investors’ demand for renewable energy. Of the unclassified funds, the best performing is the Baillie Gifford Worldwide US Equity Growth fund, which returned 191.6% over three years to the end of June.

1) Returns are not sacrificed by investing in ESG strategies. Article 9 funds have outperformed the rest in terms of returns. 2) Greenwashing will come to an end under EU SFDR thanks to heightened transparency. Fund managers will be held accountable for their ESG credentials. 3) Some investments, especially impact-oriented ones, will take time to play out but that is why they work in long-term portfolios.

KEY TAKEAWAYS

This article originally appeared in Citywire Selector’s September issue.